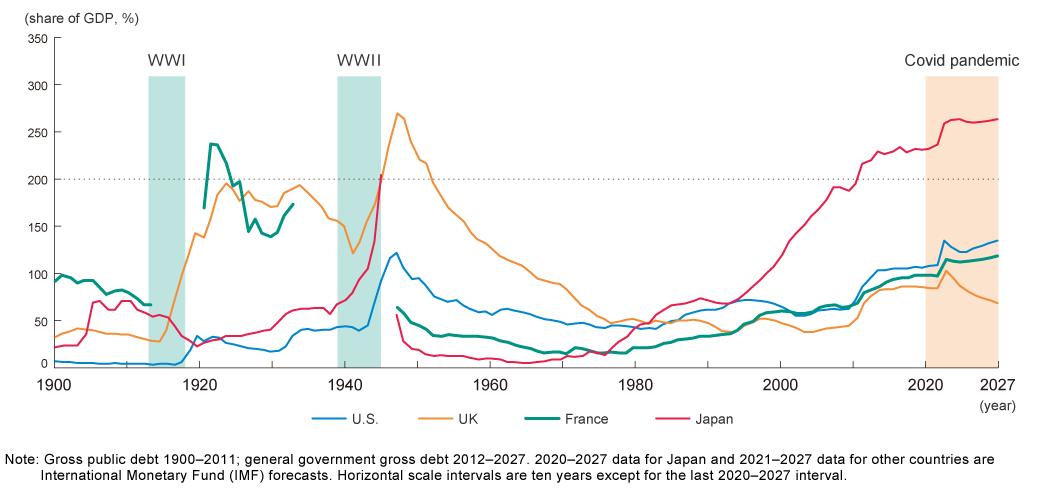

Massive economic stimulus measures during the pandemic have reached 110 trillion yen*. Government debt outstanding has increased to 260 percent of GDP, significantly above World War II levels (figure).

The increase in government debt has primarily two negative impacts on finances.

The first is heightened risk of debt crisis. When confidence in Japan’s finances declines, investors will demand higher interest rates to hold Japanese government bonds (JGBs), and consequently the actual possibility of fiscal collapse increases. According to the Ministry of Finance, a 1 percent increase in interest rates adds 3.7 trillion yen to government debt interest payments three years later1†. This is equivalent to roughly 0.7 percent of the FY2021 nominal GDP.

The second is that it becomes difficult to issue government bonds, constraining fiscal flexibility. And this could result in barriers to economic stimulus in a recession. The country will see an onset of expenditures for growing issues like fighting climate change and bolstering economic security. Looking back to the European debt crisis in the 2010s, interest rates rose for European government bonds over concerns of worsening budget positions driven by increased fiscal spending. EU governments were forced to adopt fiscal austerity notwithstanding an ongoing recession.

To date, interest rates on JGBs have remained extremely low, but the prospect of them rising is mounting due to two factors.

The increase in government debt has primarily two negative impacts on finances.

The first is heightened risk of debt crisis. When confidence in Japan’s finances declines, investors will demand higher interest rates to hold Japanese government bonds (JGBs), and consequently the actual possibility of fiscal collapse increases. According to the Ministry of Finance, a 1 percent increase in interest rates adds 3.7 trillion yen to government debt interest payments three years later1†. This is equivalent to roughly 0.7 percent of the FY2021 nominal GDP.

The second is that it becomes difficult to issue government bonds, constraining fiscal flexibility. And this could result in barriers to economic stimulus in a recession. The country will see an onset of expenditures for growing issues like fighting climate change and bolstering economic security. Looking back to the European debt crisis in the 2010s, interest rates rose for European government bonds over concerns of worsening budget positions driven by increased fiscal spending. EU governments were forced to adopt fiscal austerity notwithstanding an ongoing recession.

To date, interest rates on JGBs have remained extremely low, but the prospect of them rising is mounting due to two factors.

[Figure] Government debt outstanding in key economies

Source: Mitsubishi Research Institute, Inc. based on International Monetary Fund data

*Aggregate amount of additional spending on economic stimulus in 2020–22. Calculated using material published by the Ministry of Finance following budget approval.

†Ministry of Finance (January 2022) “Estimated Impact of FY2022 Budget on Expenditures and Revenues in Coming Years.” A 1 percent increase in interest rates applies to newly issued JGBs and does not immediately result in a 1 percent increase in the rate on JGBs outstanding, but in the long term the rate does rise by 1 percent.

Review of easy monetary policy

The first potential trigger for rising interest rates is a review of easy monetary policy. Over the past 30 years, prices have been essentially flat, and short-term policy interest rates have stayed low. Since 2016, the Bank of Japan (BoJ) has extended its policy instruments beyond just short-term rates. It now manages long-term rates by purchasing government bonds to keep yields on 10-year government bonds close to zero.

However, moves to pass through cost increases to prices have been gradually spreading recently, and household and corporate inflation expectations are rising. In addition, if 2023 spring labor offensive result in wage hikes, the price stability target of 2 percent inflation may be within reach. In that case, the BoJ may review its easy monetary policy stance. It has already widened its target range for 10-year government bond yields in December 2022.

However, moves to pass through cost increases to prices have been gradually spreading recently, and household and corporate inflation expectations are rising. In addition, if 2023 spring labor offensive result in wage hikes, the price stability target of 2 percent inflation may be within reach. In that case, the BoJ may review its easy monetary policy stance. It has already widened its target range for 10-year government bond yields in December 2022.

Rising foreign ownership of JGBs

The second factor to consider is that overseas investors own a rising share of JGBs. Historically, domestic investors have had a strong propensity to purchase and hold on to their JGBs rather than trading them, and interest rates did not tend to rise even when public finances deteriorated. As a result, market signals regarding loose fiscal discipline did not function, and there was a lack of urgency among the public and politicians regarding fiscal reconstruction, or reducing high government debt.

However, overseas investors own an increasing share of JGBs. At the end of 2020, they owned 13 percent of the total, and their share of exchange transactions rose to 67 percent. Because overseas investors manage global portfolios, as soon as they sense an increased default risk in Japan, they will demand higher interest rates to hold JGBs than domestic investors—a risk premium, in other words.

According to MRI forecasts, household savings will exceed net government financial liabilities until the mid-2040s, so in numerical terms it should be possible to absorb government debt domestically. However, if popular interest continues to turn away from savings toward investment, the amount of funds effectively available to purchase government bonds could decline.

Some research suggests that the risk of rising interest rates increases once the foreign investor ownership weighting exceeds 20 percent2. Japan is running out of time to rebuild its finances.

However, overseas investors own an increasing share of JGBs. At the end of 2020, they owned 13 percent of the total, and their share of exchange transactions rose to 67 percent. Because overseas investors manage global portfolios, as soon as they sense an increased default risk in Japan, they will demand higher interest rates to hold JGBs than domestic investors—a risk premium, in other words.

According to MRI forecasts, household savings will exceed net government financial liabilities until the mid-2040s, so in numerical terms it should be possible to absorb government debt domestically. However, if popular interest continues to turn away from savings toward investment, the amount of funds effectively available to purchase government bonds could decline.

Some research suggests that the risk of rising interest rates increases once the foreign investor ownership weighting exceeds 20 percent2. Japan is running out of time to rebuild its finances.