Russia’s invasion of Ukraine in February sent shivers down the world’s back. In a Japanese article one year ago, we outlined three factors that we saw would spur on global turbulence—a trend that is only gaining steam.

1. Volatility in world order

Though China’s emergence as a superpower means that American hegemony is coming to an end, each has a GDP that accounts for only about 20 percent of the world’s total. Meanwhile, the imposition of sanctions on Russia has strengthened solidarity among Western countries, especially the U.S., Japan, Australia, and those in Europe. However, the sanctions’ effectiveness has been diluted by China, India, and other non-Western–aligned countries’ increasing their imports of Russian energy. When the UN voted on censuring Russia in March 2022, a number of countries from the Global South abstained from voting, resulting in consensus from essentially less than half the world’s population. This made evident the complicated web of political influence behind international society consisting of three blocks: Western-aligned countries, China and Russia, and those countries caught between the two.

2. Focus on sustainability

The crisis in Ukraine has motivated many countries to hasten their shift to renewable energy in the long term as a means to ensure stable domestic energy supply. But it is also forcing a rethink of the process for transitioning. In Europe, governments are considering restarting coal-fired power plants as well as building new nuclear plants and extending the operating life of existing ones. Renewable energy comes with its own challenges too; countries run by authoritarian regimes hold a majority of the sources for materials required to fabricate equipment including storage batteries. All this makes urgent the need to find a way to achieve both carbon neutrality and national security.

3. Recalibrating capitalism

The need to rectify mounting inequality has been an ongoing issue since before the pandemic. Sights have turned to corporations to put excessive pursuit of profit behind them and build sustainable relationships with diverse stakeholders. In the U.S. and Europe, more companies are focusing on good workforce relations to retain talent amid serious labor shortages brought by the pandemic. Companies must also rethink the future of their businesses in facing economic sanctions and supply-chain disruption stemming from geopolitical conflicts due to the crisis in Ukraine.

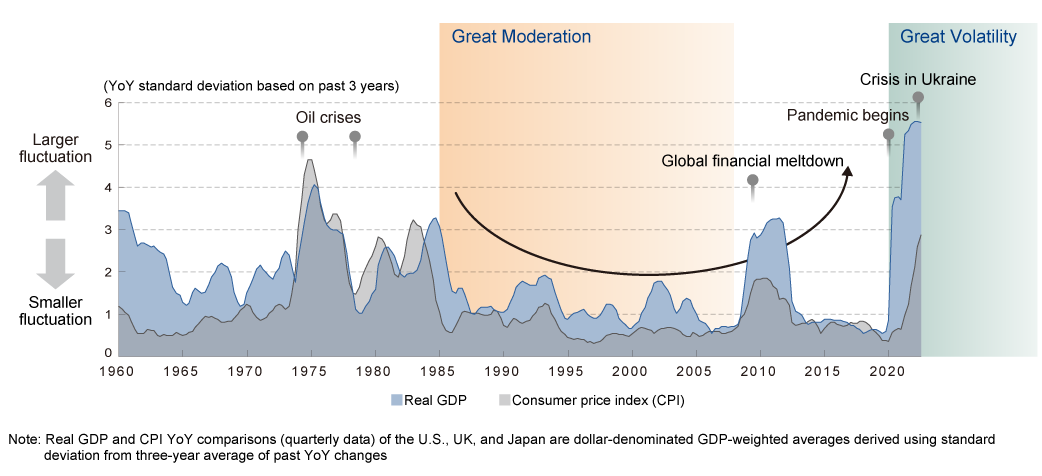

Historically high inflation has taken hold as result of these trends surfacing in the economic domain. Economies face this situation because of upward pressure on prices attributable to greater costs for resources and food, the expense of decoupling from Russia, and rising wages; these run in tangent to a jump in demand coming off of the covid pandemic. Though both supply and demand on a global level recovered progressively during 2022, high inflation and monetary tightening in mainly the U.S. and European economies put a damper on economic growth worldwide.

With economic conditions and price fluctuations like none since the 1970s, the world is inching towards an era of extreme uncertainty—an era of Great Volatility1 (Figure 1).

Historically high inflation has taken hold as result of these trends surfacing in the economic domain. Economies face this situation because of upward pressure on prices attributable to greater costs for resources and food, the expense of decoupling from Russia, and rising wages; these run in tangent to a jump in demand coming off of the covid pandemic. Though both supply and demand on a global level recovered progressively during 2022, high inflation and monetary tightening in mainly the U.S. and European economies put a damper on economic growth worldwide.

With economic conditions and price fluctuations like none since the 1970s, the world is inching towards an era of extreme uncertainty—an era of Great Volatility1 (Figure 1).

[Figure 1] Fluctuation in real GDP and CPI, 1960–2020 (U.S., UK, and Japan averages)

Source: Mitsubishi Research Institute, Inc. based on CEIC and IMF data