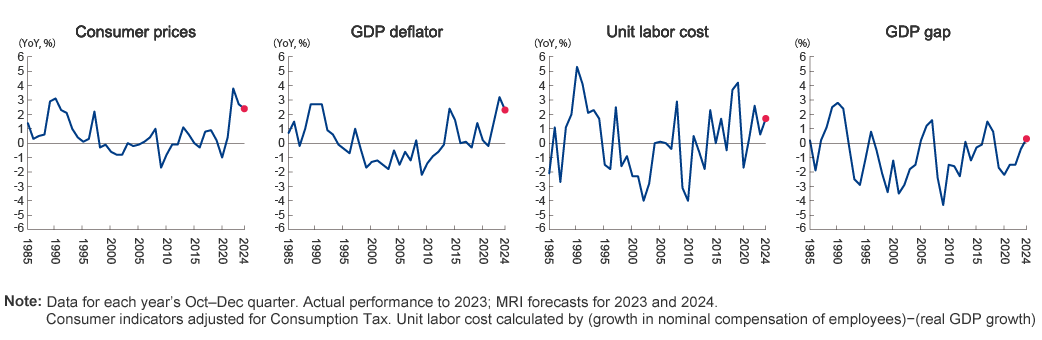

Rising prices and interest rates prompted forecasts for a major slowdown in 2023 growth, but its foundations were more solid than expected. Labor shortage-induced wage increases and easing of semiconductor-supply constraints worked positively, and each country saw consumption and capital expenditure hold their own during the year. When the final numbers are in, two-thirds of the world’s 82 significant economies are on track to have done better than their potential growth rates*.

But there’s a dark side to how firm growth is: uncertainty about the future. And it’s growing. Behind it are three structural factors.

But there’s a dark side to how firm growth is: uncertainty about the future. And it’s growing. Behind it are three structural factors.

*Calculated on GDP share in US-dollar equivalent

1. Growing multipolarity

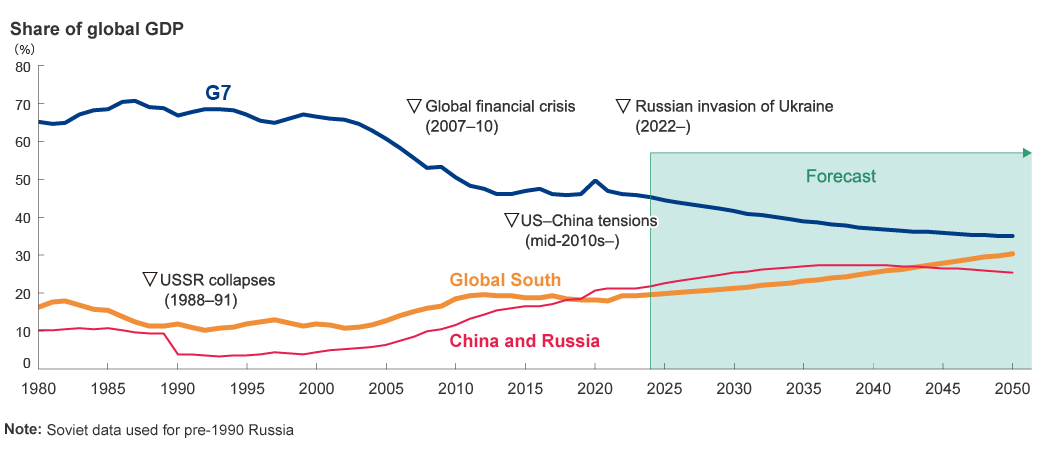

In the 1980s the G7 accounted for nearly 70% of the world’s GDP. Since then, the group’s share has dropped to 50%. Its ability to lead the world has weakened as some members have shifted their priorities to national interest as a means of quelling internal rocky politics. Moving in to fill the vacuum is the Global South—countries like India, those of ASEAN, and those in the Middle East now making their presence felt. They are carving out roles of their own, eschewing the worldviews purported by the G7, China, and Russia. Making up a third pole, we forecast them to account for nearly as much of global GDP in 2050 as the G7 (Figure 1). In a world polarized around these three groups, it will be all the harder to find common ground for working out challenges they need to tackle together.

Figure 1: Global GDP share by country grouping

Source: Mitsubishi Research Institute forecasts for 2024 onward, International Monetary Fund for 1980–2023

2. Supply-chain vulnerability

Growing geopolitical rivalry is increasingly baring vulnerabilities in existing supply chains built on economic rationale. The advance of globalization means that countries have grown highly interdependent in numerous ways, including for sensitive technologies and essential resources. As this multipolarization progresses, countries have become more economically dependent on states with different political systems and values. The flip side of this is that these relationships are ripe for abuse if one country decides to leverage them to gain advantage over another, for instance by halting trade in a good over a dispute. Russia’s cutting off natural gas flows to European countries and the energy crisis it precipitated are still fresh in memory, and the US is tightening restrictions on exports and investments that could contribute to China’s ability to manufacture advanced semiconductors.

3. High reliance on debt

According to the Bank for International Settlements (BIS), the world’s non-financial sector private and public debt has ballooned to some 2.5 times global GDP. Markets have been increasingly concerned about government debt, whose rise quickened during the pandemic. On top of the UK’s “Truss shock”* of 2022, the US’s credit rating was downgraded† in 2023, the first time in a dozen years. China and other emerging powers are seeing the pace of debt expand beyond the rate of economic growth. And further, structural pressures to expand government budgets—for things like decarbonization, economic security, and military expenditures—are rising. These developments fuel concerns over potential destabilization of financial systems due to greater losses at financial institutions if countries should default under their oversize debt loads, as well as worries about postponement of necessary investment when capital is diverted to cover repayment obligations.

*A spike in interest paid on UK government bonds prompted by market concern over the repercussions of major tax cuts announced by the Truss government. The incident led to the prime minister’s and treasury secretary’s resignations

†Fitch Ratings, a major ratings agency, downgraded US debt to AA+, one notch below its highest, AAA rating